¶ Description

Create a Kolmogorov-Smirnov curve after applying a model.

¶ Parameters

¶ Parameters tab

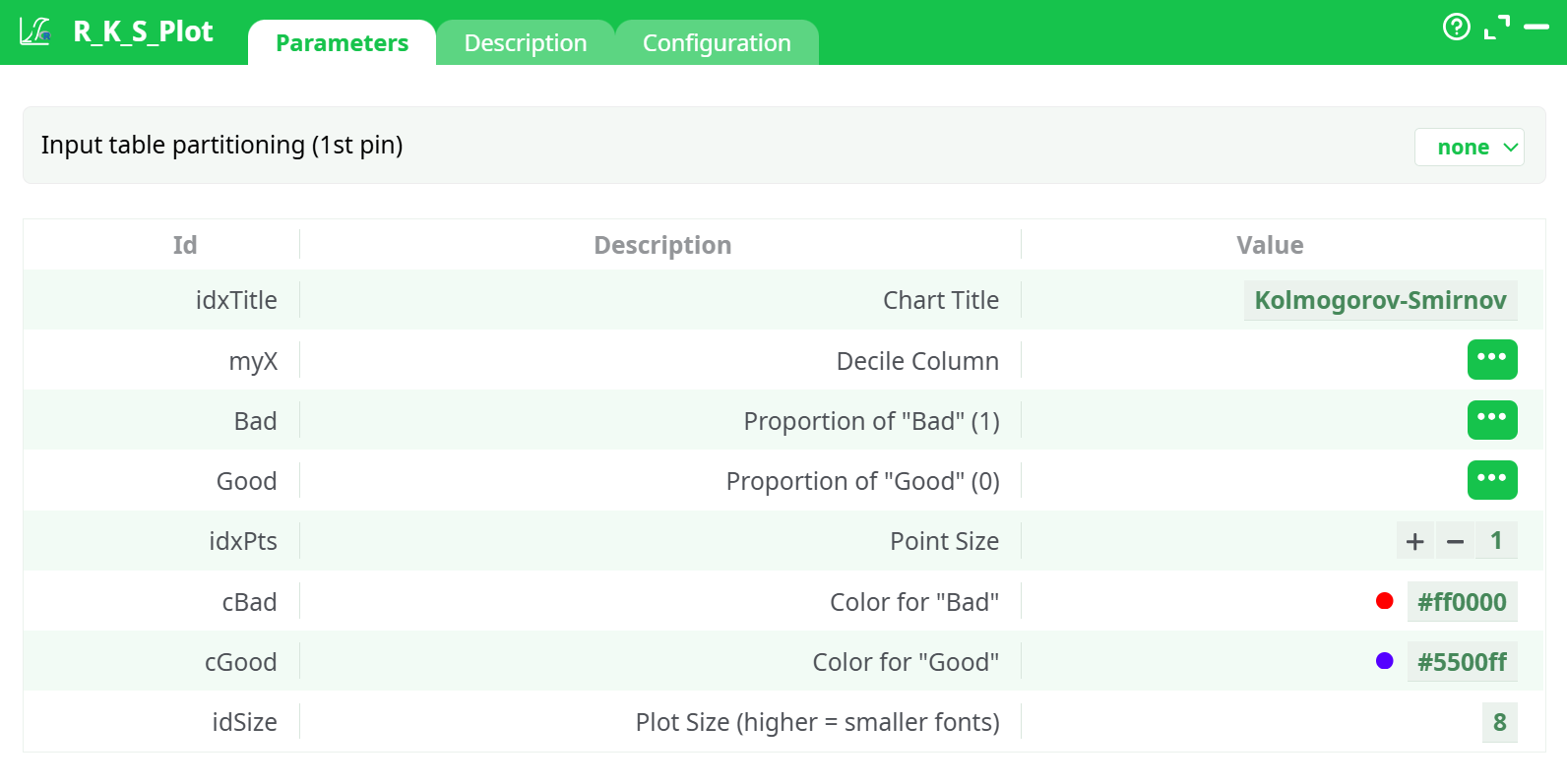

Parameters:

- Chart Title

- Decile Column

- Proportion of "Bad" (1)

- Proportion of "Good" (0)

- Point Size

- Color for "Bad"

- Color for "Good"

- Save Image in PNG? (empty field=no save)

- Plot Size (higher = smaller fonts)

¶ Description tab

Parameters:

- Script name

- Short description

- Revision

- Description

¶ Configuration tab

See dedicated page for more information.

¶ About

Create a Kolmogorov-Smirnov curve after applying a model. The input data consists of an aggregated table (usually deciles) in which we have computed:

- Proportion of “bad” in each decile (usually the target)

- Proportion of “good” in each decile

- The decile

This curve is often used in credit risk analysis, but is – generally speaking – not a very robust way to evaluate a model as it assumes a normal distribution of the scores which is not appropriate if you work with actual transactional data. Some authors suggest that a logartimic transformation can improve it, but this would only be appropriate if using a logistic regression (which depends on transformed scores, and in general WoE), but not with any ML algortithm that do not use this transformation.

¶ Use Cases

- Evaluate scorecard model effectiveness

- Detect class separation across population bins

- Visualize classification accuracy for binary labels