¶ Description

Build and compare TimeSeries on sequential data.

¶ Parameters

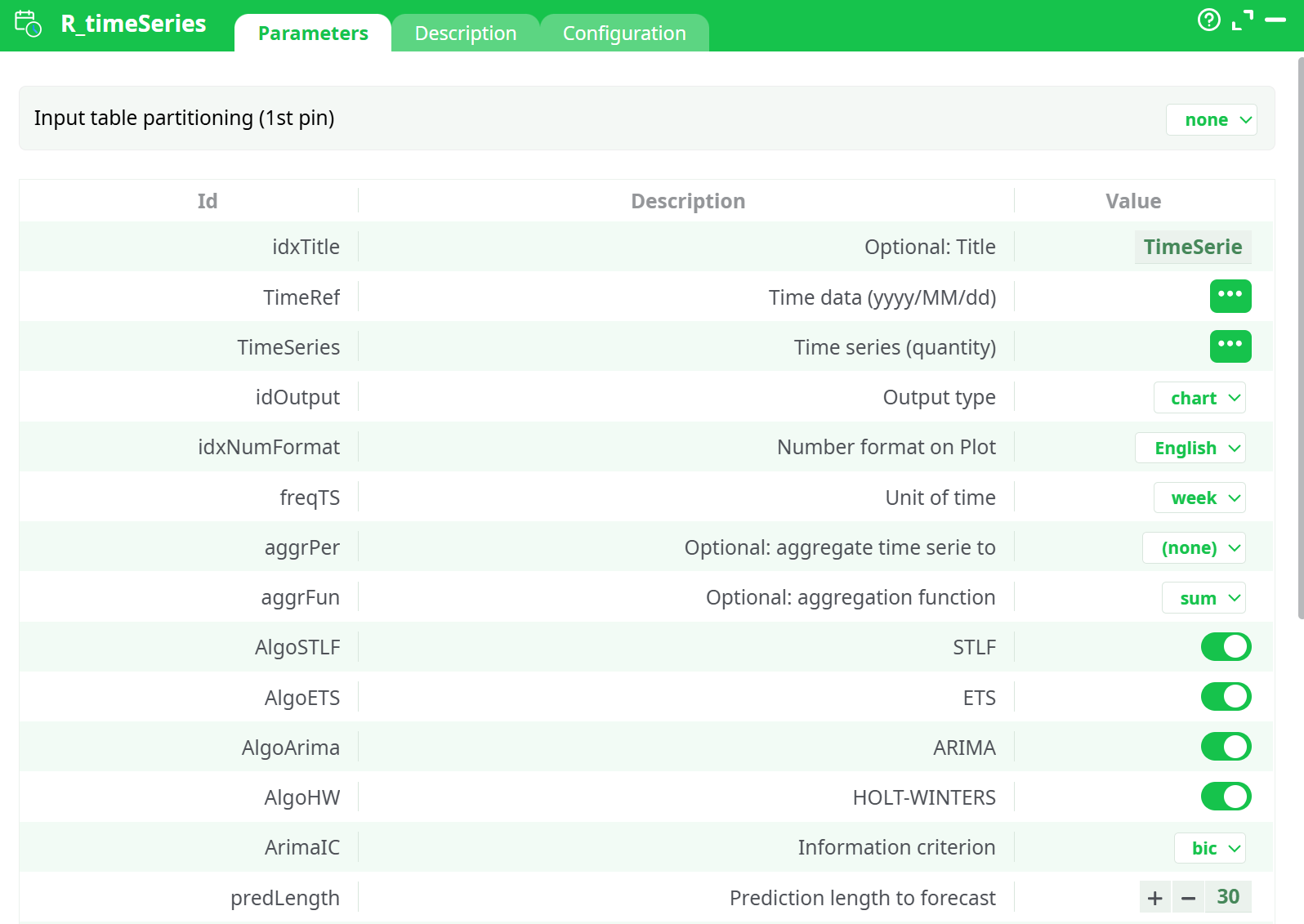

¶ Parameters tab

Parameters:

- Title (optional)

- Time data (yyyy/MM/dd)

- Time series (quantity)

- Number format on Plot

- Unit of time

- Aggregate time serie to (optional)

- Aggregation function (optional)

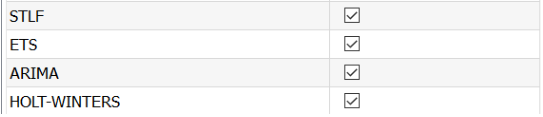

- STLF

- ETS

- ARIMA

- HOLT-WINTERS

- Information criterion

- Prediction length to forecast

- Confidence interval

- Time series color

- Decomp: trend smoothing periodicity

- Decomp: season degree

- Decomp: trend degree

- Decomp: robust

- Holt winters alpha

- Holt winters beta

- Holt winters gamma (seasonal)

- Holt winters seasonality

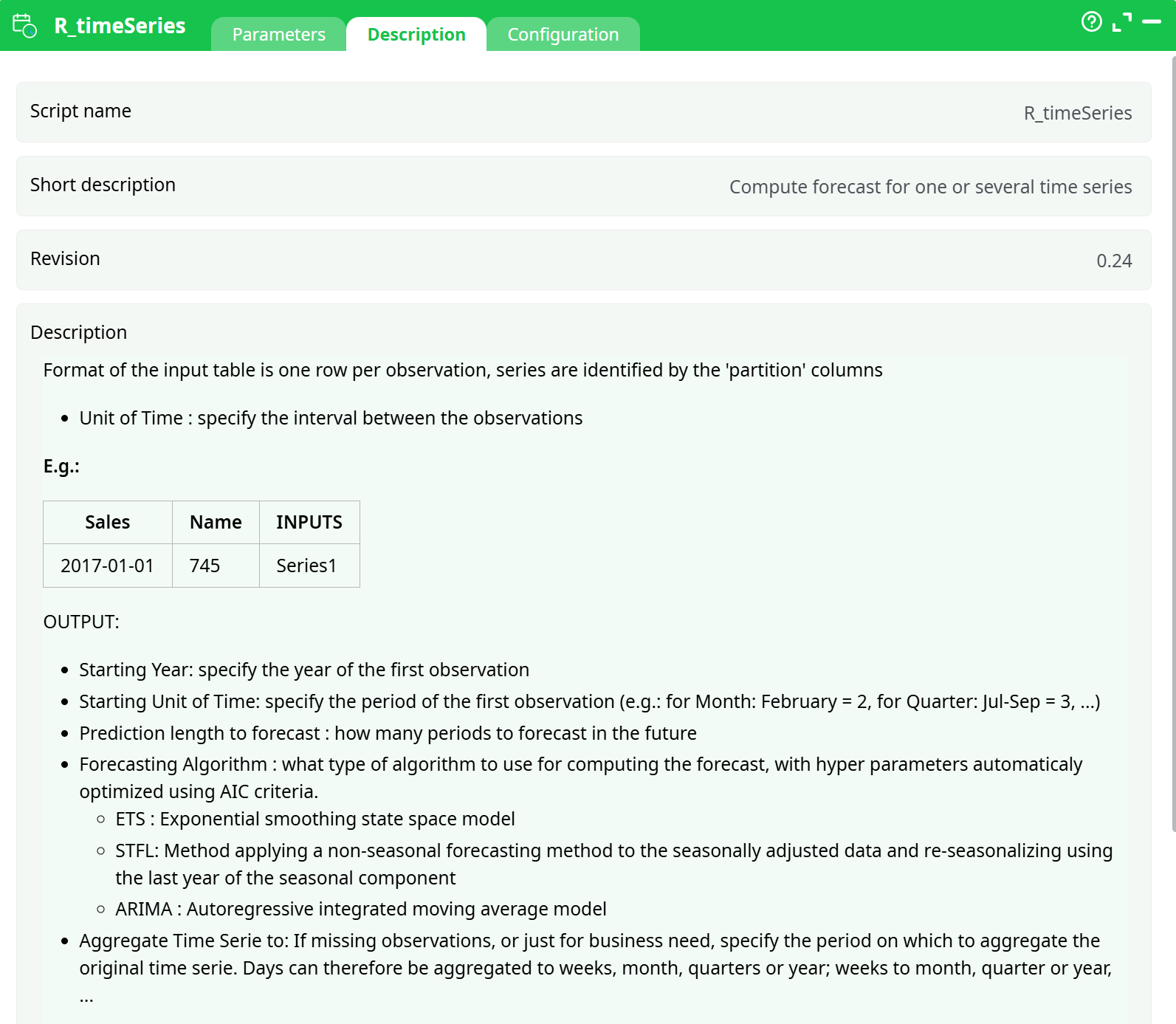

¶ Description tab

Parameters:

- Script name

- Short description

- Revision

- Decription

¶ Configuration tab

See dedicated page for more information.

¶ About

Use this node to compute ETS, STLF, ARIMA and Holt-Winters models.

At the very least, you need to have two series: one with dates (YYYY-MM-dd or YYYY/MM/dd or any separators, as long as the order and number of characters is respected).

Then, you need to specify the time units between observations (Unit of Time). ETL will attempt to do it for you, and if it doesn’t match the data, it will recode it. But it’s always better to help the software.

Then, specify on which time frame you wish to run the analysis (Aggregate Time Series) to get smoother – and usually better – results. You can specify whether you want the sum or the average computed

Then, you can optionally uncheck the algorithms you don’t want to run (because you know what you are doing... or leave them all checked and let R figure out which one works.

When you run the algorithms, make sure you force ETL to write cache: right click on the object and set the option

You can set some advanced parameters for the decomposition, for ARIMA and for Holt Winters.

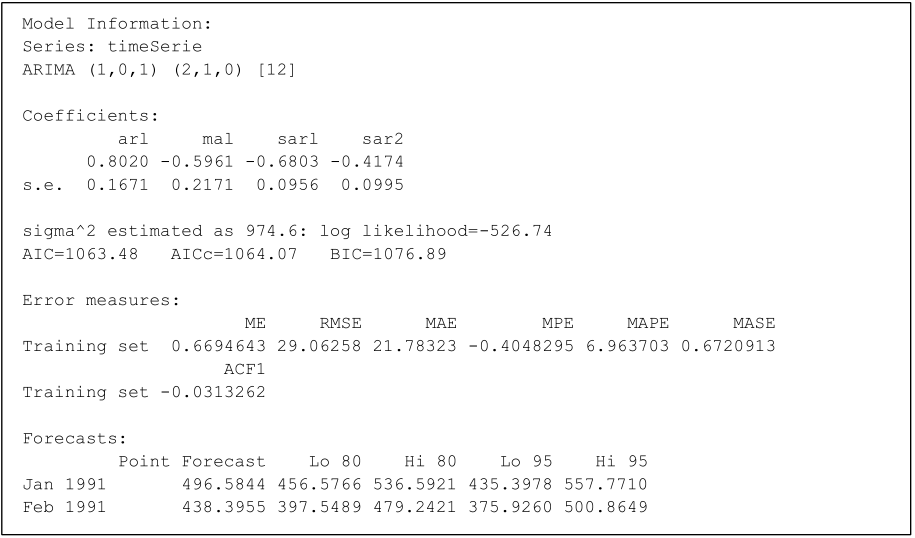

- Arima: Information Criterion: By default, you should use BIC as a criterion, as it will perform better if heterogeneity is large (Aho, 2014) , but AIC an AICC are also available and should be checked as other criterion may yield better models. As a reminder, the key difference between AIC and BIC is that BIC penalizes stronger the number of parameters, and this is often desirable.

Consider Θ̂ is the max likelihood estimates of the model parameters, logℓ(Θ ̂ ) is the log likelihood of the model, 𝑞 is the number of parameters and 𝑜 the number of observations. - AIC: Akaike Information Criteria = −2logℓ(Θ̂ ) + 2𝑞

- AICC: Aikake for Small Samples 𝐴𝐼𝐶 + 2𝑝(𝑝+1)/𝑛−𝑝−1

- BIC: Bayesian Information Criteria. −2logℓ(Θ̂ ) + 𝑞log𝑜

Thus, when you have few observations (as often in timeseries) AICC would be the most conservative (and preferred) test to apply. When you have “a lot” of points (over 100), BIC or AIC would be appropriate. The details of the model are available in the log:

- Trend Smoothing Periodicity: this parameter will set how many periods are used to smooth the trend line. If you put a small number, you will have a very non-linear trend, if you put a large number you will get something more stable. If you leave it at 0, the default value of R for ( t.window) is used: nextodd(ceiling((1.5*period)/(1-(1.5/s.window))))

- Decomp: Season Degree: (0/1) degree of the function for seasonality. Set to 0 if you don’t think there is seasonality

- Decomp: Trend Degree: (0/1) degree of the function for trend. Set to 0 if you don’t think there is trend

- Decomp Robust: Set if you want to use a robust method

- Holt Winters alpha, Beta and Gamma: Set starting values to help avoid local optima.

Outputs

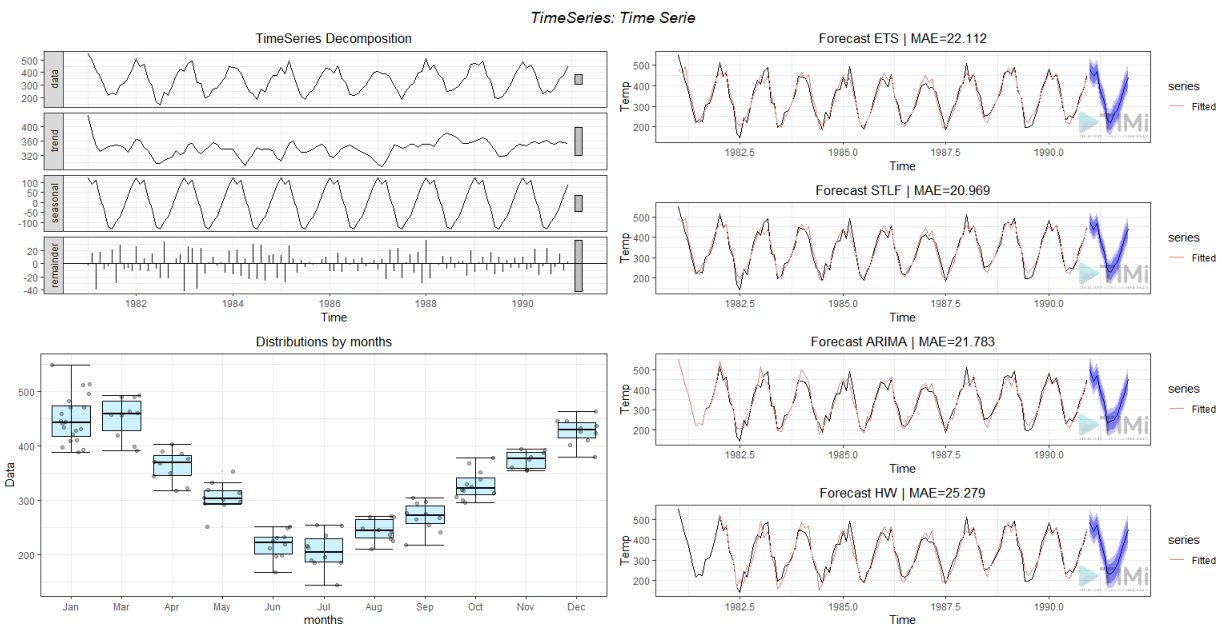

If you are lucky (you have a data structure that fits the time series framework) you will get the following plot:

Here, we can observe the decomposition of trend, seasonality and error of the data, a action plot showing the distribution (error) per time unit, and the results of each algorithm.

You can pick the one with the lowest MAE, of look at the diagnostics for more KPIs:

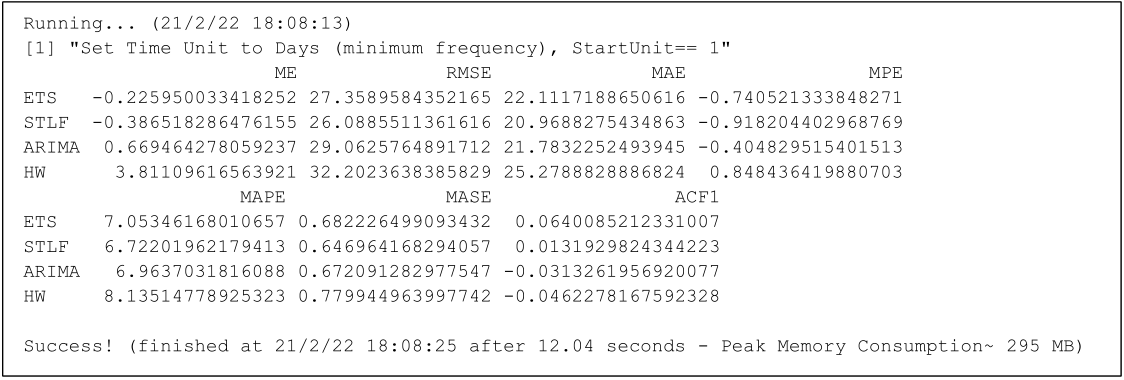

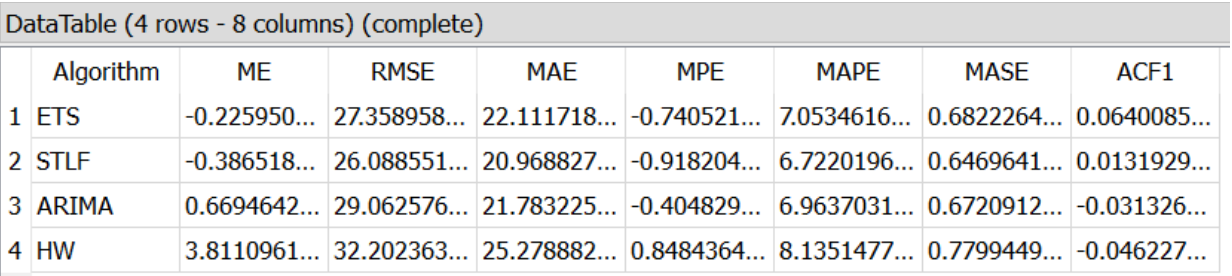

The same information is available in the second output pin:

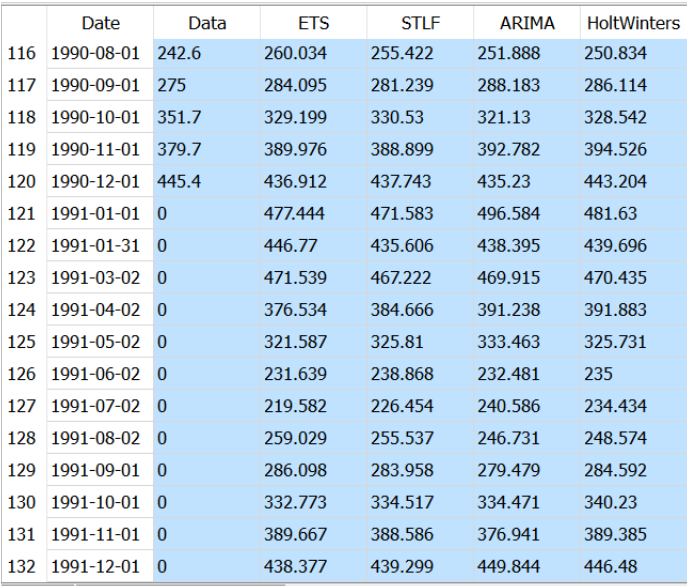

The first output pin will give you the computed estimates for each observation, as well as the prediction for all successful algorithms (for those, the original observation will be set to 0)

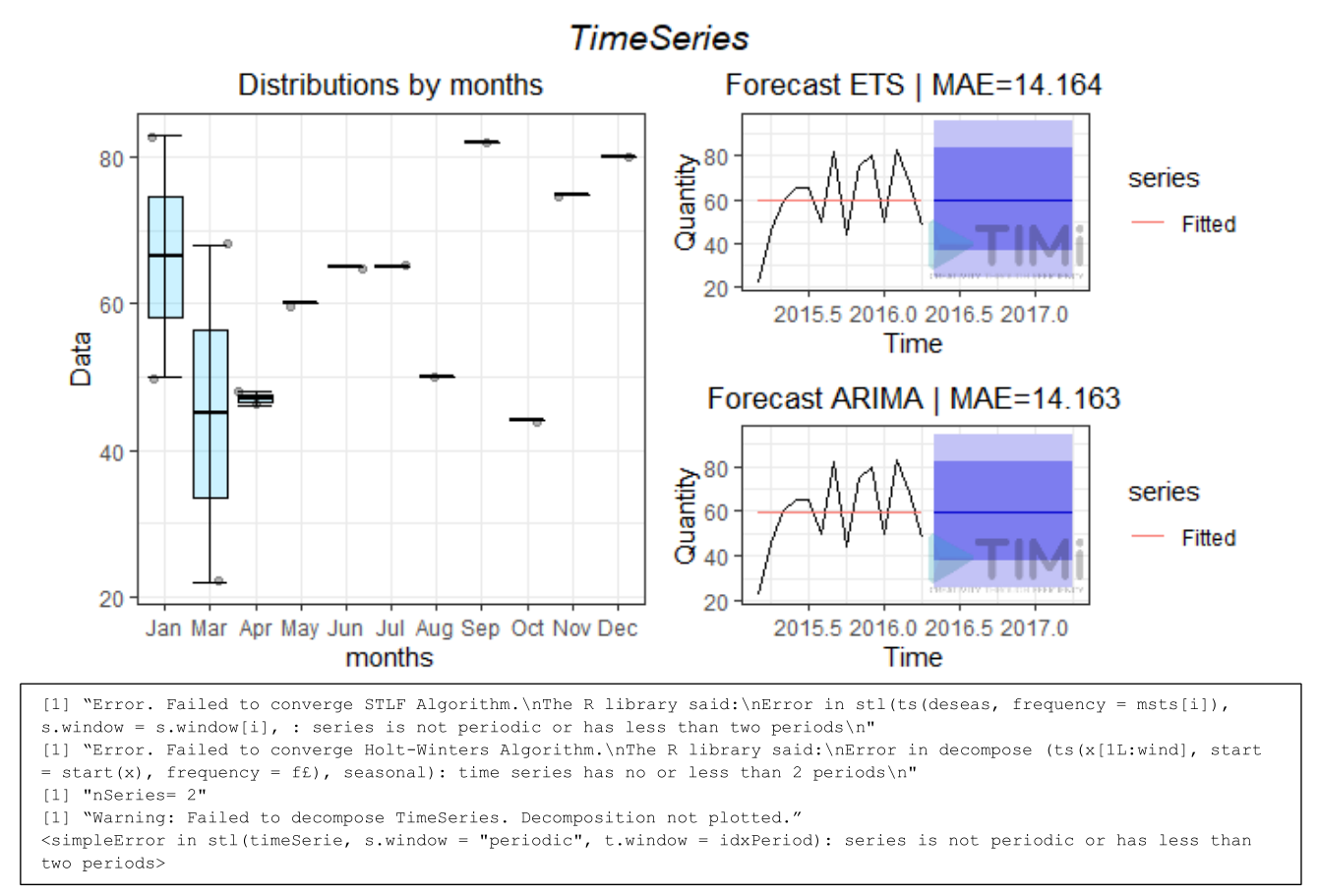

If we are unlucky, the time series will fail to decompose, and /or you may end up with constant estimates (when the algorithms doesn’t simply fail). In this case, only the action plot and timeSeries plots will be returned. You will also see and error message in the log telling you what happened (in R dialect)

In this case, STLF and Holt Winters failed, Arima and ETS failed without crashing, and simply return a constant prediction. The reason here is obvious: there is not enough data to find cycles!